Introduction

A Roth IRA for beginners in 2026 is a retirement savings account where you contribute money you have already paid taxes on — and your investments grow completely tax-free forever. In 2026, you can contribute up to $7,000 per year, and every dollar of growth you withdraw in retirement is 100% tax-free.

If you are just starting to invest, a Roth IRA for beginners is one of the smartest first moves you can make. This guide covers everything — what it is, how it works, 2026 limits, and exactly how to open one today.

Disclaimer: This article is for informational and educational purposes only. It does not constitute personalized financial advice. Please consult a licensed financial advisor before making investment decisions.

What Is a Roth IRA for Beginners?

A Roth IRA (Individual Retirement Account) is a special investment account with a powerful tax benefit. You pay taxes on the money before you put it in. After that, the government leaves it alone — forever.

Think of it this way. Imagine a magic jar. Everything you earn inside that jar grows without the IRS touching it. When you retire and take money out, it is all yours — no taxes owed.

That is exactly what a Roth IRA does for your retirement savings. It is one of the most beginner-friendly investment tools available to Americans today.

How Does a Roth IRA Work?

Understanding the basics of a Roth IRA for beginners comes down to three simple rules.

Rule 1 — You contribute after-tax money. Unlike a traditional IRA, you do not get a tax deduction today. However, that small sacrifice pays off massively later.

Rule 2 — Your money grows tax-free. Inside the Roth IRA, your investments — whether index funds, ETFs, or S&P 500 funds — grow year after year with zero annual taxes.

Rule 3 — Withdrawals in retirement are 100% tax-free. After age 59½ and with the account open for at least 5 years, every dollar you withdraw — including all the growth — comes out completely tax-free.

One more thing beginners love: You can withdraw your contributions (not earnings) at any time, for any reason, penalty-free. The IRS already taxed that money once — they will not touch it again.

2026 Roth IRA Contribution Limits

For 2026, the IRS has set the following contribution limits:

| Age | 2026 Contribution Limit |

|---|---|

| Under 50 | $7,000 per year |

| Age 50 and older | $8,000 per year (includes $1,000 catch-up) |

Important rules to remember:

- You can contribute to a Roth IRA any time between January 1 and the tax filing deadline (April 15, 2027 for the 2026 tax year)

- You can spread contributions across the year — monthly, quarterly, or all at once

- You cannot contribute more than your earned income for the year

- The limit applies across all your IRAs combined (Roth + Traditional)

Source: IRS.gov — irs.gov/retirement-plans/roth-iras

2026 Roth IRA Income Limits

A Roth IRA for beginners has one important restriction — income limits. If you earn too much, you cannot contribute directly to a Roth IRA.

Here are the 2026 income phase-out ranges:

| Filing Status | Full Contribution | Phase-Out Range | No Contribution Allowed |

|---|---|---|---|

| Single / Head of Household | Under $150,000 | $150,000 – $165,000 | Above $165,000 |

| Married Filing Jointly | Under $236,000 | $236,000 – $246,000 | Above $246,000 |

| Married Filing Separately | $0 | $0 – $10,000 | Above $10,000 |

What if you earn too much? There is a legal workaround called the Backdoor Roth IRA. You contribute to a Traditional IRA first, then convert it to a Roth IRA. This is legal and widely used by high-income earners. However, it has tax implications — consult a licensed financial advisor or CPA before doing this.

Source: IRS Official 2026 Roth IRA Rules → “Verify the latest 2026 limits directly on IRS.gov.“

Roth IRA vs. Traditional IRA — Which Is Better for Beginners?

This is one of the most common questions in a Roth IRA for beginners guide. Here is the clearest comparison:

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax on contributions | After-tax (no deduction now) | Pre-tax (deduction now) |

| Tax on growth | Tax-free | Taxed on withdrawal |

| Tax on withdrawals | Tax-free (after 59½ + 5 years) | Ordinary income tax |

| Required withdrawals at 73? | No | Yes (RMDs apply) |

| Income limits | Yes | No (but deduction limits apply) |

| Best for… | Beginners, younger earners | Higher earners expecting lower retirement tax |

The bottom line for beginners: If you are in your 20s, 30s, or even 40s — and you expect your income to grow over time — a Roth IRA is almost always the better choice. You lock in today’s lower tax rate. Your money grows for decades. And you pay zero taxes in retirement.

“Already thinking about where to put that money? Read our full guide on investing $1,000 for beginners.”

How to Open a Roth IRA for Beginners — Step by Step

Opening a Roth IRA takes about 10–15 minutes online. Furthermore, it is completely free at most major brokerages.

Step 1 — Check your eligibility Confirm you have earned income and your MAGI falls within the 2026 income limits above.

Step 2 — Choose a brokerage These three are the most beginner-friendly options in 2026:

| Brokerage | Minimum to Open | Commission | Best For |

|---|---|---|---|

| Fidelity | $0 | $0 | Beginners — best overall tools |

| Charles Schwab | $0 | $0 | Excellent mobile app |

| Vanguard | $0 | $0 | Best for long-term index investors |

Step 3 — Complete the online application Have these ready: Social Security Number, government-issued ID, and your bank account details. Most applications take 10–15 minutes.

Step 4 — Fund your account Transfer money from your bank. You can start with as little as $1 at Fidelity or Schwab thanks to fractional shares.

Step 5 — Choose your investments This is the step most beginners skip — and it is the most important. A Roth IRA is just a container. What you put inside determines how it grows. (See the next section.)

Step 6 — Set up automatic contributions Even $50 or $100 per month adds up massively over decades. Set it and forget it.

Best Investments to Put Inside Your Roth IRA for Beginners

Most beginners make one critical mistake: they open a Roth IRA and leave the money sitting in cash. Cash earns almost nothing. Your Roth IRA needs actual investments inside it to grow.

Here are the best beginner-friendly options:

S&P 500 Index Funds — The Gold Standard

An S&P 500 index fund gives you instant ownership in 500 of America’s largest companies — Apple, Microsoft, Google, Amazon, and more. Over the last 30 years, the S&P 500 has returned an average of approximately 10.4% annually.

Top S&P 500 options for your Roth IRA:

| Fund | Expense Ratio | Type |

|---|---|---|

| VOO (Vanguard S&P 500 ETF) | 0.03% | ETF |

| FXAIX (Fidelity 500 Index Fund) | 0.015% | Mutual Fund |

| SPY (SPDR S&P 500 ETF Trust) | 0.09% | ETF |

Past performance does not guarantee future results.

Target-Date Index Funds — Simplest Option for Beginners

If you want to set it and forget it completely, a target-date fund is the easiest choice. You pick the year closest to when you plan to retire — say, 2055 — and the fund automatically adjusts its mix of stocks and bonds as you get older.

Fidelity Freedom Index Funds and Vanguard Target Retirement Funds are two excellent, low-cost options.

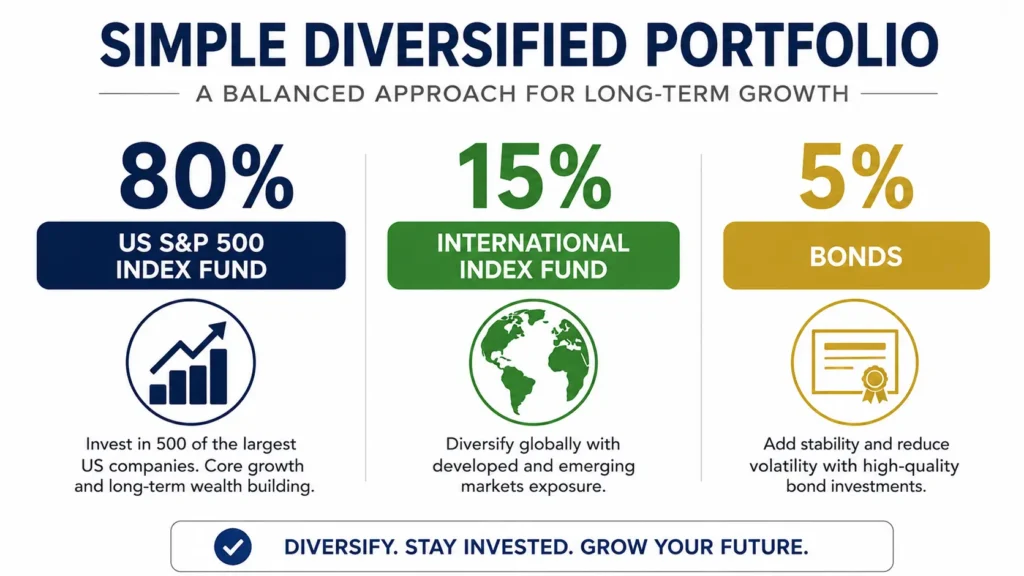

Diversify Your Portfolio with a Simple 3-Fund Mix

As your balance grows, consider diversifying your portfolio with three simple funds:

- US Total Market Index Fund (core holding)

- International Index Fund (global diversification)

- Bond Index Fund (stability — add when within 10–15 years of retirement)

This simple approach beats most actively managed funds over a 15–20 year period.

Roth IRA Withdrawal Rules — What You Need to Know

Understanding withdrawal rules is essential in any Roth IRA for beginners guide. Specifically, the rules differ depending on what you withdraw.

Withdrawing Contributions (Your Original Money)

You can withdraw your contributions at any time, at any age, with no taxes and no penalties. The IRS already taxed that money when you earned it.

Withdrawing Earnings (Your Growth)

Earnings are tax-free and penalty-free only when:

- Your account has been open for at least 5 years, AND

- You are age 59½ or older

If you withdraw earnings before meeting both conditions, you generally owe income tax plus a 10% early withdrawal penalty on those earnings.

Special Exceptions (No Penalty on Earnings)

Even before 59½, you can withdraw earnings penalty-free (though taxes may still apply) for:

- First-time home purchase (up to $10,000 lifetime limit)

- Permanent disability

- Death (paid to beneficiaries)

- Qualified education expenses

The key takeaway: Treat your Roth IRA as untouchable until retirement. The longer you leave it alone, the more tax-free growth compounds inside it.

FAQ — Roth IRA for Beginners 2026

Q1: What is a Roth IRA and how does it work for beginners?

A Roth IRA is a retirement account where you contribute after-tax money, and all growth is tax-free. For beginners, it is one of the best starting points because withdrawals in retirement are 100% tax-free. Open one at Fidelity, Schwab, or Vanguard for free, invest in an S&P 500 index fund, and let compound growth work over decades.

Q2: How much can I contribute to a Roth IRA in 2026?

In 2026, the Roth IRA contribution limit is $7,000 per year for those under age 50. If you are 50 or older, the limit increases to $8,000 with the catch-up contribution. You have until April 15, 2027 to make your 2026 contribution. Source: IRS.gov.

Q3: What is the income limit for a Roth IRA in 2026?

Single filers can make a full contribution with income under $150,000 in 2026. The contribution phases out between $150,000 and $165,000. Married couples filing jointly phase out between $236,000 and $246,000. Above those limits, the backdoor Roth IRA strategy may allow contributions.

Q4: Should a beginner choose a Roth IRA or a Traditional IRA?

For most beginners — especially those in their 20s or 30s — a Roth IRA is the better choice. You pay taxes now at your current lower rate, and all future growth is tax-free. A traditional IRA makes more sense if you expect to be in a lower tax bracket in retirement than you are today.

Q5: What should I invest in inside my Roth IRA as a beginner?

The simplest and most effective starting investment is a low-cost S&P 500 index fund like VOO or FXAIX. Both charge under 0.1% annually and give you instant diversification across 500 US companies. Alternatively, a target-date index fund automates everything for complete hands-off investing.

Q6: Can I have both a Roth IRA and a 401(k)?

Yes, absolutely. Having a 401(k) at work does not affect your Roth IRA contribution limit. The 2026 Roth IRA limit ($7,000) and 401(k) limit ($23,500) are completely separate. Financial advisors often recommend contributing enough to get your full 401(k) employer match first, then maxing out your Roth IRA.

Conclusion + CTA

A Roth IRA for beginners in 2026 is one of the most powerful tools available for building long-term, tax-free wealth. The steps are simple: check your eligibility, open an account at Fidelity, Schwab, or Vanguard, put your money into a low-cost S&P 500 index fund, and contribute consistently over time.

The earlier you start, the more decades of tax-free compounding you unlock.

Your next step: Now that you understand how a Roth IRA works, the next question is — what exactly should you put inside it? Learn everything about choosing the right S&P 500 index fund for your Roth IRA.

📌 Also Read: [Invest $1,000 for Beginners — 5 Smart Moves That Actually Work ]

Financial enthusiast with 5 years of experience in the US market trends and personal wealth management